The low period of settling a loan means that the monthly premiums tend to be significant

It should not surprise your whenever a financial institution set a repayment title from 15 if not 20 years once they commit to funds your MH buy.

Luckily that one may become settling your own home smaller and save your self far more in the long term.

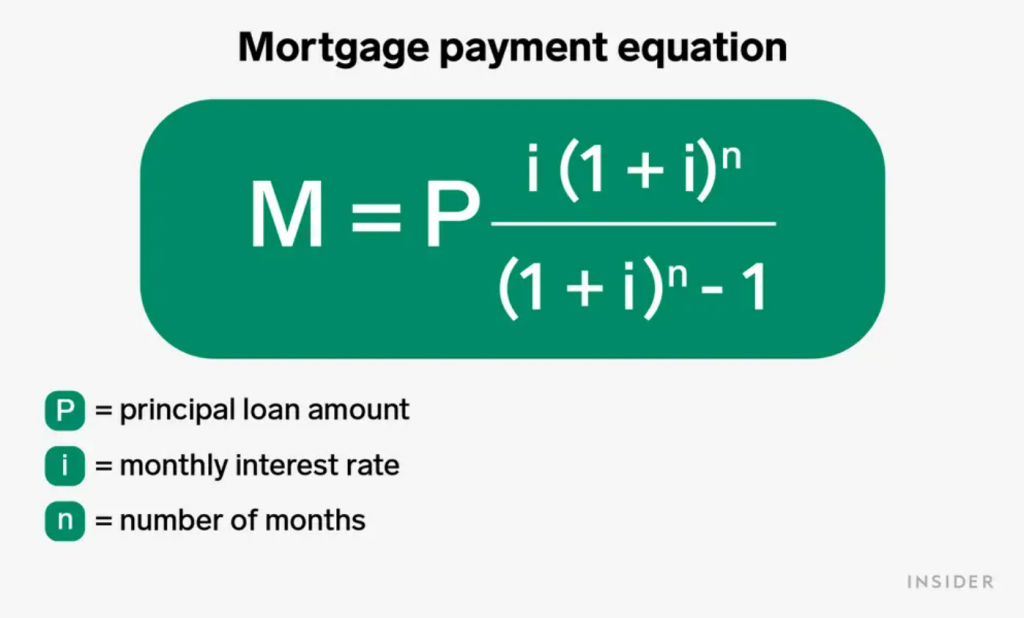

The fresh amortization agenda will provide you with a writeup on just how payments might possibly be split up amongst the desire and you will dominant on Virtual assistant cellular financial.

Va Mobile Domestic Assistance

The latest Experts Issues rolled out the recommendations to own categorizing cellular or are formulated homes tools into the . Qualified mobile residential property need certainly to meet with the following conditions:

Become mounted on a long-term site that abides by the official guidelines with the minimal with the-site weight and you may effectiveness strong winds.

Feel developed as per the are produced house construction and you will coverage requirements passed of the HUD and you will sustain HUD certificates and you may tags.

Adhere to each other regional and you will state rules to the are produced residential property, especially if the structure is actually missing HUD tags or are changed.

- Possess at least floor area of 700 square feet having a good double-broad equipment and you may 400 square feet for an individual-wider device.

You will still feel the chance to have the cellular family redesignated while the property in case it is currently categorized while the a great chattel.

There are also to share the ground arrangements and you can needs of your construction when you’re getting financing to the a manufactured house you to hasn’t been sited yet ,.

Exactly what Qualifies due to the fact Real property

Ahead of being attached with the brand new designated web sites, manufactured land is actually ferried into social courses. After arranged on the ground, it initiate because the auto just before transitioning in order to real property.

A good number of people don’t discover is that MHs try classed because chattels otherwise vehicles before getting installed on a selected lot.

The auto or chattel designation is actually issued in it due to the fact residents need to pay the fresh new DMV to move them doing. As MH finds the site, you have to do a title removing to get it reclassified of an automible to help you real property.

Based a state, reclassifying your own MH could possibly get include a small paperwork. The relevant authorities requires one to fill out some variations and you can pay running fees.

Since procedure is completed, the MH usually meet the requirements due to the fact real property and become entitled to home loan products like Virtual assistant cellular lenders.

Until the financial techniques your loan, they’re going to require that you confirm their rights toward residential property in which the MH might be mounted.

Land/Package Considerations to possess Mobile House

Some thing you can also know after you listen to the phrase mobile house is a leisure vehicles depending contained in this a park otherwise good community-hired park.

Although modern relaxation car are designed to provide smoother traditions requirements, they aren’t qualified within the Va mobile mortgage program. Simply because their tires continue to be unchanged, while the house a lot of them people into the is leased.

New Experts Situations requires you to very own this new house in which your own MH is positioned about how to qualify for a mobile house loan. The newest land identity will help persuade the lender you permanently intend to attach a made domestic into the a designated plot.

Things to Understand Va-accepted Loan providers

Lenders can be procedure a cellular financial versus entry the loan processing recommendations into the Experienced Items for further underwriting review.

However, a state or government agencies should glance at lenders (mortgage and you may mortgage companies, financial institutions, and you can funds and you will discounts relationships).

They should have legitimate recognition provided by Pros Issues according to Virtual assistant cellular mortgage brokers system criteria.