Which are the Affairs that Find Home loan Eligibility?

Want to get a home loan? Before you proceed to end all the nitty-gritty, you need to look at the financial eligibility. As per the qualifications out of a home loan, A man need to be a resident of Asia and must be more than 21 years of age when you’re obtaining our home financing. With regards to the lender otherwise standard bank your local area applying to possess home financing, they want a number of records which might be needed to end up being used. To understand more info on Financial Qualifications, let’s browse the certain products that dictate your residence mortgage Qualifications:

Age:

Your house loan eligibility is estimated to possess a certain several months named tenure. Your own tenure hinges on your actual age, plus capability to pay it off during the a certain months. The skill of a young applicant to spend right back their mortgage is different from regarding a heart-old otherwise resigned individual. home loan borrowers in lot of phase of the lifetime face pressures which might be different. Finance companies imagine eg products while evaluating applications. Of the believe and you may cost management better, you are able to beat new barriers people of your age category deal with, and acquire the most basic loans in Edgewater alternative available.

Employment Condition:

The employment position can be very important since your earnings. Working within the an MNC otherwise a reputed personal otherwise individual markets providers enables you to way more credible as the a borrower. And, if you find yourself a personal-working private, then lenders are more likely to present an effective sanction to the versatile terms and conditions compared to the some one which have an unstable occupations or company.

Income:

This does not need subsequent explanation. Your earnings highly impacts exactly how many currency banking companies and you will economic institutions are willing to give you. The better your income, the more what kind of cash banks was willing to provide your. All the loan providers assert that applicants should have a certain number of earnings getting entitled to home financing. This, needless to say, varies continuously with your job. Your home loan qualification is actually computed based on your revenue.

Qualification & Experience:

In the event your instructional back ground and you can really works feel try unbelievable, the possibilities of the lending company sanctioning your home financing is large. For example, whenever you are an effective salaried staff member, you must have no less than 2 to 3 several years of performs feel to get eligible for home financing. Also, when you’re a personal-functioning personal, your business have to be operational for many age, with sufficient dollars profits and you will profits. Tax statements should have also been filed from inside the business’s title. The academic credentials and functions feel predict profession improvements and you can balances fairly well.

Version of A job:

The sort of work will have an impression in your home financing qualifications. Banking institutions love whether you’re salaried, or whether you’re a self-Functioning Top-notch (SEP) otherwise a self-Operating Low-Top-notch (SENP). The newest qualifications requirements vary depending on the kind of work. Regular business change make a difference your clients of getting a house financing.

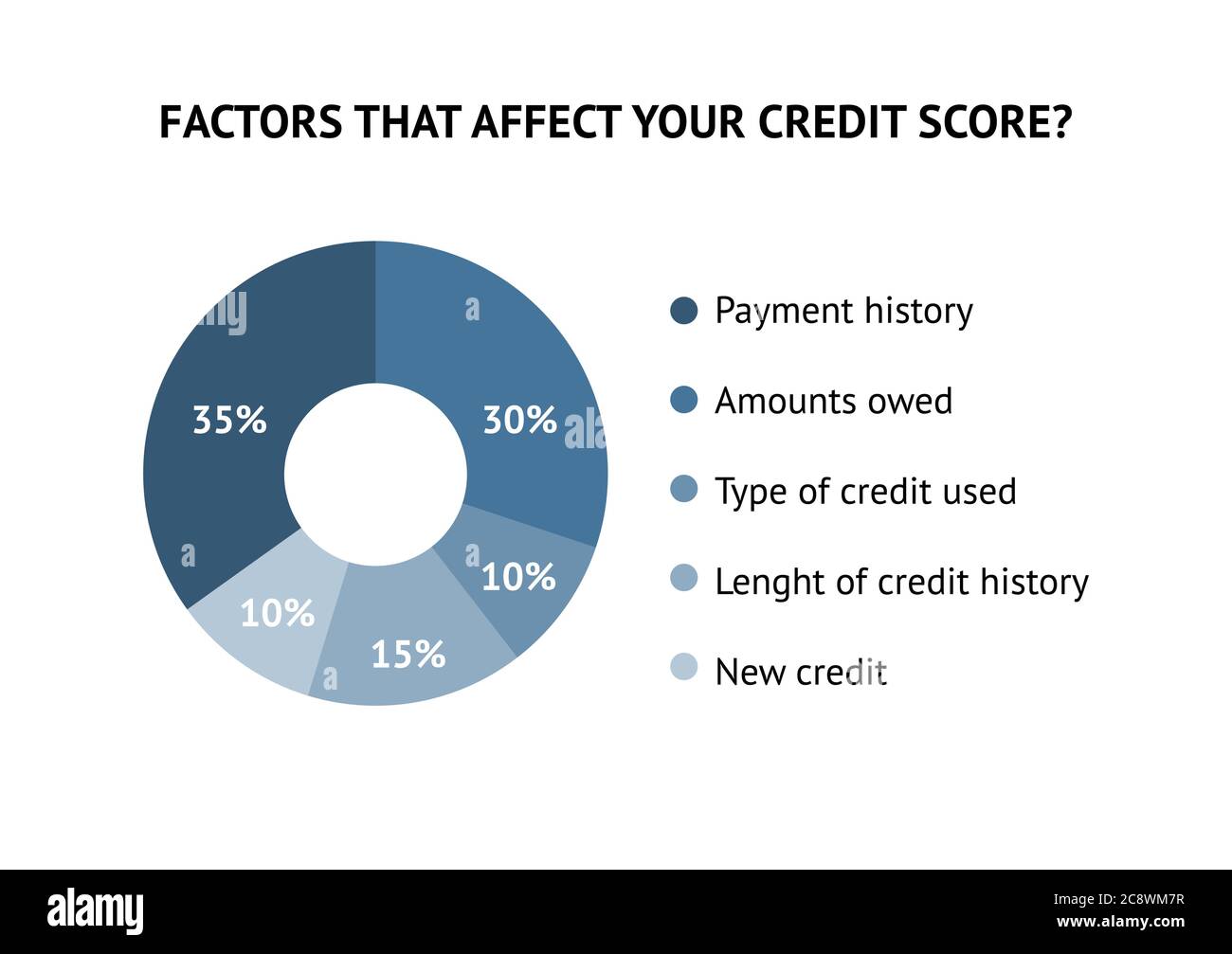

Credit rating:

A credit rating gives a very clear photo for the lender because the to help you the way you enjoys handled their debts while having exactly how capable you are off repaying your house loan. Ahead of sanctioning the mortgage, loan providers measure the credit history of your own candidate, so it vital that you keep up proper credit score. Regrettably, if you have a very reasonable credit rating or of numerous pre-existing finance, the application could also be declined.

This is simply not only the primary and the appeal components of your own EMI that you need to have to worry about. It’s also wise to need certainly to plan the money to own margin currency towards the home loan. The lender loans merely 80 per cent of your market value out-of the house named (LTV) we.elizabeth. Loan-to-Value Ratio (90 % in case there are home loans below Rs 30 lakhs). The fresh new debtor need certainly to strategy the 20% (otherwise 10 % as case are) of your market value of the house. This new down payment you happen to be prepared to build are certain to get a massive impact on your property financing qualifications.

Sector Financing Rates:

The newest Set-aside Lender from India’s (RBI) policies and market credit/interest rates features a massive effect on the debt and you can improves. Rates of interest dictate the worth of credit money. The higher the rate of interest, the greater is going to be the value of your house mortgage. In simple terms, ascending lending rates will boost rising cost of living and you may dissuade borrowing from the bank, and work out discounts more attractive. Declining rates build borrowing more desirable.

Tips Calculate Your house Financing Eligibility:

Though this type of variables may differ out-of bank so you can bank and an excellent pair banks eters to help you fill out, whatever you would like to do is, open the fresh new calculator web page and type in or find the pursuing the

- Your local area

- Years or day off birth

- Find your own internet monthly money

- Choose other money

- Discover the financing period you might favor